Thursday, April 9, 2026

Blog

Prime Minister addresses the 14th India-France CEOs Forum

Prime Minister Shri Narendra Modi and the President of France, H.E. Mr. Emmanuel Macron jointly addressed the 14th India-France CEOs Forum today in Paris. The forum brought together CEOs from a diverse group of companies from both sides, focusing on sectors such as defence, aerospace, critical and emerging technologies, infrastructure, advanced manufacturing, artificial intelligence, life-sciences, wellness and lifestyle, and food and hospitality.

Prime Minister in his address noted the expanding India-France business and economic collaboration and the impetus it has provided to the strategic partnership between the two countries. He highlighted India’s attractiveness as a favored global investment destination, based on its stable polity and predictable policy ecosystem. Talking of the reforms announced in the recent budget, PM noted that the insurance sector was now open for 100% FDI and civil nuclear energy sector for private participation with focus on SMR and AMR technologies; customs rate structure was rationalized; and simplified income tax code was being brought in to enhance Ease of Living. Referring to the government’s commitment to continue ushering in reforms, he noted that a high-level committee for regulatory reforms had been constituted to establish trust based economic governance. In the same spirit, more than 40,000 compliances had been rationalized in the last few years.

Prime Minister invited French companies to look at the immense opportunities offered by the India growth story, in the defense, energy, highway, civil aviation, space, healthcare, fintech and sustainable development sectors. Underlining global appreciation and interest in India’s skills, talent and innovation and in its newly launched AI, Semiconductor, Quantum, Critical Minerals and Hydrogen missions, he called upon French enterprises to partner India for mutual growth and prosperity. He outlined the importance of active engagement in these sectors, reaffirming the commitment of both nations to fostering innovation, investment, and technology-driven partnerships. Full remarks of Prime Minister may be seen here

External Affairs Minister Dr. S. Jaishankar, alongside the Minister for Europe and Foreign Affairs of France, H.E. Jean-Noël Barrot, and the Minister of the Economy, Finance, and Industrial and Digital Sovereignty of France, H.E. Eric Lombard also addressed the Forum.

India Energy Week 2025 showcases India’s clean cooking gas model: A blueprint for the Global South

India Energy Week 2025 showcases India’s clean cooking gas model: A blueprint for the Global South

Union Minister of Petroleum and Natural Gas, Shri Hardeep Singh Puri chaired a Ministerial Roundtable on Clean Cooking on the second day of India Energy Week 2025. Shri Puri highlighted India’s remarkable success in ensuring universal access to clean cooking gas through targeted subsidies, strong political will, digitisation of distribution networks by Oil Marketing Companies (OMCs), and nationwide campaigns promoting cultural shifts towards clean cooking.

The session brought together representatives from Brazil, Tanzania, Malawi, Sudan, Nepal, and industry leaders including the International Energy Agency (IEA), Total Energy, and Boston Consulting Group (BCG).

Shri Puri emphasized that India’s model is not only successful but also highly replicable in other Global South nations facing similar energy access challenges. The Union Minister noted that under India’s Pradhan Mantri Ujjwala Yojana (PMUY), beneficiaries receive LPG access at a highly affordable cost of just 7 cents per day, while other consumers can avail themselves of clean cooking fuel at 15 cents per day. This affordability has been a game-changer in driving widespread adoption.

During the discussion, international representatives shared their experiences and challenges in expanding access to clean cooking solutions. Hon. Dkt. Doto Mashaka Biteko, Deputy Prime Minister and Minister of Energy, Tanzania outlined its strategy to enable 80% of households to transition to clean cooking by 2030, leveraging subsidies and a mix of energy sources, including LPG, natural gas, and biogas. However, he acknowledged significant challenges, including financing constraints, the high cost of infrastructure, and the need for regulatory reforms to encourage private-sector participation.

H.E. Dr. Mohieldien Naiem Mohamed Saied, Minister of Energy and Oil, Sudan, emphasised the need for private sector engagement to bridge gaps in LPG supply, as the country still imports a significant portion of its energy needs. Encouraging local cylinder production and ensuring cost-effective imports remain key hurdles in achieving broader adoption. Representatives of Rwanda and Nepal shared their efforts in reducing firewood dependency through electric stoves and biogas expansion.

Mary Burce Warlick, Deputy Executive Director of IEA noted that India’s success offers valuable lessons for other countries, particularly in tackling challenges related to affordability, access, and infrastructure. She further emphasised the role of concessional financing and public-private partnerships (PPP) in expanding clean cooking access globally. Addressing cultural acceptance and regulatory adjustments, such as tax reductions, were also highlighted as crucial measures for large-scale adoption.

Rahool Panandiker, Partner at Boston Consulting Group (BCG) highlighted India’s clean cooking transformation, underscoring its strong political commitment, effective subsidy targeting, and robust public awareness campaigns. He further credited India’s Oil Marketing Companies (OMCs) for enabling last-mile LPG delivery through digital platforms, making adoption seamless. Panadiker also underscored the need for refining the cylinder refill model to ensure sustained usage and balancing affordability with economic sustainability.

Responding to the potential of solar cookers in expanding clean cooking technologies across the Global South, Shri Puri highlighted that IOCL’s advanced solar cookers, featuring integrated solar panels, are priced at approximately $500 per unit with no additional costs over their lifecycle. The Union Minister added that while the current price point remains a challenge for widespread adoption, leveraging carbon financing and collaborating with the private sector could drive costs down, making solar cooking a viable alternative for millions.

This initiative aligns with India’s broader efforts to diversify clean cooking options beyond LPG, reinforcing the country’s commitment to reducing reliance on traditional biomass fuels and cutting carbon emissions.

Shri Puri concluded the discussion by reaffirming India’s commitment to supporting energy access initiatives worldwide. He underscored that the Indian model, backed by smart subsidies and sustainable policies, provides a scalable solution for other developing nations striving to achieve clean cooking access. He stressed that achieving universal clean cooking access is not merely an economic imperative but a moral one, given the severe health and environmental impacts of traditional biomass cooking.

This roundtable reaffirmed India’s position as a global leader in energy transition and clean cooking solutions, setting the stage for greater international cooperation in achieving universal access to clean energy.

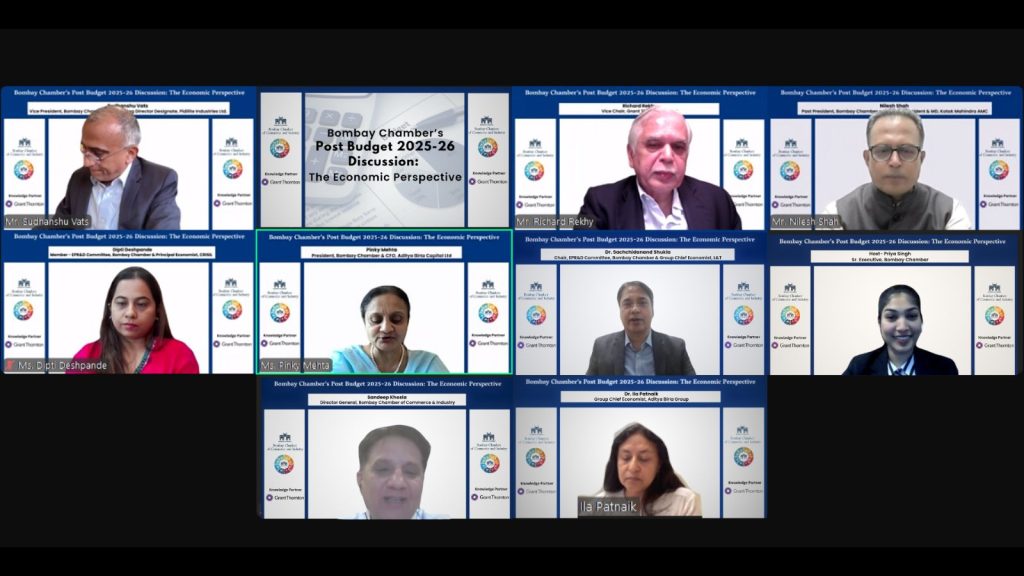

Bombay Chamber Hosts Post-Budget 2025-26 Webinar: An Economic Perspective

Bombay Chamber Hosts Post-Budget 2025-26 Webinar: An Economic Perspective

Mumbai, February 4, 2025 – The Bombay Chamber of Commerce & Industry, under the aegis of its Economic Policy Research & Development (EPR&D) Committee hosted a post-budget discussion on the economic perspective following the Union Budget 2025-26, presented by Finance Minister Nirmala Sitharaman on February 1, 2025.

The webinar commenced with a welcome address by Pinky Mehta, President of the Bombay Chamber and CFO of Aditya Birla Capital Ltd., who highlighted the budget’s focus on strengthening private sector investments, boosting household sentiment, and enhancing middle-class purchasing power. She noted that Finance Minister Sitharaman reaffirmed the government’s commitment to inclusive growth through targeted initiatives for the poor, youth, farmers, and women, while also underscoring MSMEs as the “second engine” of the economy. Key budget highlights included the Prime Minister Dhan-Dhaanya Krishi Yojana, which aims to enhance agricultural productivity across 100 districts, and the announcement of five National Centres of Excellence for skilling, supporting India’s ambition to become a global manufacturing hub.

The panel discussion, moderated by Dr. Sachchidanand Shukla, Chair of the EPR&D Committee at the Bombay Chamber and Group Chief Economist at L&T, featured distinguished experts, including Dr. Ila Patnaik, Group Chief Economist at Aditya Birla Group; Nilesh Shah, Past President of the Bombay Chamber and Group President & MD at Kotak Mahindra AMC; Sudhanshu Vats, Vice President of the Bombay Chamber and Managing Director Designate at Pidilite Industries.; Dipti Deshpande, Principal Economist at CRISIL; and Richard Rekhy, Vice Chair at Grant Thornton Bharat.

Discussions focused on tax reforms, economic growth, fiscal discipline, and global trade. Shah highlighted the need for better tax compliance and expressed optimism for a more favourable tax regime in the coming years. Deshpande noted that despite tax relief measures, income tax collections are projected to grow by 20.6 percent, driven by structural changes, compliance, and digitalisation. She also highlighted the government’s commitment to fiscal prudence, noting that the fiscal deficit has been reduced to 4.4 percent and remains on track to fall below 4.5 percent in 2025-26. Revenue spending cuts, strong tax collections, and PSU dividends are key drivers of this fiscal consolidation, reinforcing India’s long-term economic stability.

Dr. Patnaik stressed the importance of removing the inverted duty structure to create a level playing field for Indian industries and noted that policy changes are advancing the Make in India initiative. Vats described the budget as balanced and forward-looking, citing the one lakh crore rupees tax rebate as a bold move to stimulate middle-class consumption and drive growth in manufacturing, services, and GST revenues. Addressing global trade concerns, Shah emphasised the need for India to engage in strategic partnerships to avoid negative impacts from ongoing trade tensions.

Rekhy pointed out that while middle-class spending is rising, challenges such as food inflation, underemployment, and regulatory complexities persist. He highlighted the importance of skilling initiatives to support India’s goal of becoming a global talent hub.

The panellists agreed that the Union Budget 2025-26 maintains a strong balance between fiscal prudence and economic growth, with continued policy implementation and regulatory reforms being key to sustaining long-term stability.The session concluded with a vote of thanks by Sandeep Khosla, Director General of the Bombay Chamber.

By: Raj Singh

No Comments

Budget 2025-26 empowers MSMEs, Middle class as engines for industrial growth

Budget 2025-26 empowers MSMEs, Middle class as engines for industrial growth

In her eighth consecutive Union Budget 2025-26, Finance Minister Nirmala Sitharaman delivered a Budget which reflected the government’s strategic focus on empowering MSMEs and implementing comprehensive reforms to foster industrial growth and economic development in India. The Budget also introduced historic income tax changes aimed at benefiting the middle class. This Budget seeks to invigorate private sector investments, uplift household sentiments, and strengthen the purchasing power of India rising middle class, the finance minister stated.

In her address, Sitharaman outlined the government focus on ten key areas of development, emphasising support for the poor (Garib), youth (Yuva), farmers (Annadata), and women (Nari). Sitharaman also recognised MSMEs as the second engine of the economy, highlighting their significant role in India industrial growth. Currently, over one crore registered MSMEs contribute 37% of manufacturing output and 45% of exports, positioning India as a global manufacturing hub.

Reactions from Bombay Chamber Leaders:

Pinky Mehta, President Bombay Chamber and CFO of Aditya Birla Capital Ltd:

This Budget has a focus on double ‘M’ – MSMEs and the Middle Class. The investment limit for MSMEs has been raised by 2.5 times, reflecting the government’s commitment to strengthening this sector. This move will encourage higher capital investment and expansion among MSMEs. Moreover, a significant increase in the credit guarantee cover for MSMEs, doubling it from ₹5 crore to ₹10 crore, is expected to facilitate an additional ₹1.5 lakh crore in credit over the next five years, thereby improving access to finance for small businesses. The relief for the Middle class with no income tax payable up to ₹12 lakh under the new tax regime is expected to increase disposable income, thereby stimulating demand across various sectors, including FMCG and the automotive industry.

Rajiv Anand, Sr. Vice President, Bombay Chamber and Deputy Managing Director, Axis Bank:

The path to fiscal consolidation is welcome. The income tax cut will help the middle class and consumption.

Sudanshu Vats, Vice President, Bombay Chamber and Managing Director Designate, Pidilite Industries Ltd.

I would like to compliment Hon Finance Minister for a good balanced budget with clear focus on driving consumption while staying the course on fiscal consolidation. The two key features have been reduction in personal Income Tax leaving more money in the hands of Indian consumers and the introduction of PM Dhan Dhaanya Krishi Yojana for 100 districts – a more holistic approach to address the Agriculture sector.

Nilesh Shah, Past President, Bombay Chamber and Group President & MD, Kotak Mahindra AMC Ltd:

The budget delivers on the expectations of Triveni sangam of reduction in fiscal deficit, support to urban consumption through tax cuts and increase in Capex through center, state and PSUs allocation. The budget is forward looking with six year guidance on reducing debt to GDP ratio, allocation to deep tech fof of Rs 10,000 crore, maritime fund of Rs 25000 crore for ship buildingand Rs 20000 crore For small modular nuclear reactors and Focus on Education through digital books, broadband connectivity, increase in medical and IIT seats and Atal tinkering labs.

Sudhir Kapadia, Past President Bombay Chamber and Senior Advisor, EY

This budget has given one of the most expansive giveaways on the personal income tax front, with the government foregoing an unprecedented Rs 1 lakh crore in direct tax revenues. With this, the government has shown that it is listening to the middle class voices. This will also bring about a spurt in disposable income, benefiting the economy. The big announcement on the new income tax bill that will be introduced next week is much welcome. The new bill will be simpler and easier for taxpayers to understand. The formation of a high level panel for Regulatory Reforms to review regulations, certifications, licences, and permissions in the non- financial sector is another signal that we are open to business.

Key Highlights of the Budget 2025-26

Economic Growth & Development

● India remains the fastest-growing major economy.

● The budget prioritises accelerated growth and inclusive development.

● Emphasis on private sector investments and enhanced household confidence.

10 Focus Areas

● Prioritising Garib (poor), Yuva (youth), Annadata (farmers), and Nari (women).

● Focus on taxation, urban development, mining, financial sector, power, and regulatory

reforms.

Agriculture & Rural Development

● PM Dhan Dhaanya Krishi Yojana to improve agricultural productivity in 100 low-yield

districts.

● Expansion of storage infrastructure at the panchayat level.

● Special initiatives for pulse crops (urad, tuar, masoor).

● Establishment of a Makhana Board in Bihar to boost local production.

MSME & Industrial Growth

● Investment and turnover limits for classification will be enhanced by 2.5 times, encouraging expansion and employment generation.

● Credit guarantee cover will be increased from ₹5 crore to ₹10 crore for micro-

enterprises, leading to an additional ₹1.5 lakh crore in credit over the next five years.

Healthcare & Education

● 75,000 new undergraduate medical seats to be added in the next five years.

● Day-care cancer centers to be established in all district hospitals.

● 50,000 Atal Tinkering Labs to be set up in government schools.

Infrastructure & Logistics

● India Post to be transformed into a major public logistics organisation.

● New urea plant in Assam with a capacity of 12.7 lakh metric tons.

● Reactivation of three dormant urea plants in Eastern India.

Entrepreneurship & Women Empowerment

● ₹2 crore term loan scheme for 5 lakh first-time women, SC, and ST entrepreneurs.

● MSME credit guarantee cover expanded to ₹20 crore, with reduced guarantee fees.

Technology & Innovation

● Establishment of the National Institute of Food Technology, Entrepreneurship, and

Management in Bihar.

● Bharatiya Bhasha Pustak Scheme to promote Indian language digital books for

education.

● Five national skilling centers to support the ‘Make for India, Make for the World’

initiative.

Energy & Sustainability

● Nuclear Energy Mission targets 100 GW of nuclear energy by 2047.

● Amendments to the Atomic Energy Act to facilitate private sector participation.

Social Welfare & Financial Inclusion

● Enhanced support for gig and online platform workers via identity cards and the e-

Shram portal.

● Revamped PM SVANidhi scheme with higher loan limits and UPI-linked credit cards for

street vendors.

Unique contributions of women are vital to India’s maritime strength: Shri Shantanu Thakur

Unique contributions of women are vital to India’s maritime strength: Shri Shantanu Thakur

Launches flagship programmes—’Sagar Mein Yog’ – Complete Wellness Programme” and ‘Sagar Mein Samman’

Union Minister of State, Ministry of Ports, Shipping and Waterways, Shri Shantanu Thakur said that the unique contributions of women are vital to India’s maritime strength and women seafarers embody resilience and excellence on the global stage.

Launching officially the logos and themes of “Sagar Mein Yog – Complete Wellness Programme” and “Sagar Mein Samman”, respectively at The Shipping Corporation of India (SCI), Mumbai, on Thursday, he pointing out that the initiative is crucial for ensuring that female seafarers, who often face distinct challenges while working far from home, are celebrated and supported.

Further, he emphasised the profound connection between yoga and Indian heritage, noting the programme’s significance for our nearly 3 lakhs plus active seafarers, who face unique challenges while serving far from home. As global ambassadors of India, our seafarers would exemplify the nation’s resilient spirit and maritime excellence, he added.

Inspired by the Honourable Prime Minister’s Maritime India Vision 2030, “Sagar Mein Samman” is a transformative initiative aimed at recognising and enhancing the role of women in the maritime industry. The programme echoes fostering respect and empowerment and seeks to ensure that women seafarers can thrive and navigate their careers with dignity and pride. Further, Sagar Mein Yog focuses on wellness at every stage by integrating yoga and wellbeing practices into maritime training and operations at stages such as Pre-Sea, At-Sea, and Post-Sea for ensuring seafarers remain resilient, balanced and prepared for every journey.

Shri Shyam Jaganathan, Director General of Shipping, emphasised that under the visionary leadership of Hon’ble Prime Minister Shri Narendra Modi, Maritime India Vision 2030 symbolises hope by uplifting women seafarers and steering India toward maritime excellence. The “Sagar Mein Samman” initiative was born from this vision, aiming to enhance the respect and recognition afforded to women in the maritime community. Further, he added that the Prime Minister’s vision symbolizes hope-empowering oceans, uplifting seafarers and steering India toward maritime excellence.

By tracking health outcomes, Sagar Mein Yog will refine and expand its offerings to meet seafarers’ evolving needs. The initiative is expected to reduce medical emergencies, lower healthcare costs, and decrease turnover rates, creating a supportive maritime environment. Sagar Mein Yog stands as a symbol of our unwavering commitment to the holistic well-being of our seafarers before, during and after their voyages.

The launch event was attended by stakeholders and seafarers reaffirming India’s commitment to setting a global benchmark for seafarer health. From the vast Indian Ocean to our shores of progress, India’s maritime legacy continues to drive growth.ly.

SEBI has zero tolerance for RPT violations, will levy fines on directors and compliance officials alike

SEBI has zero tolerance for RPT violations, will levy fines on directors and compliance officials alike

Bombay Chamber, Mumbai: The Securities and Exchange Board of India (SEBI) has a zero-tolerance policy on related party transaction (RPT) violations. Not just that, the kind of orders being passed of late against compliance officers is far-reaching. The Bombay Chamber of Commerce & Industry has learnt that SEBI is not only passing orders and levying fines on compliance officers but also writing to the Institute of Company Secretaries of India to take disciplinary action against the member.

Speaking at the Related Party Transaction (RPT) seminar held recently by the Bombay Chamber of Commerce & Industry in Mumbai, Bharat Vasani, Chairperson, Legal Affairs & IPR Committee, Bombay Chamber of Commerce & Industry and Senior Advisor – Corporate Laws at Cyril Amarchand Mangaldas, said, SEBI is not only making the director and compliance official accountable but also penalising them.

“I recently came across a case wherein a fine of Rs 2 crore was levied on the executive director to whom the company secretary was reporting. Additionally, the company secretary was fined Rs 3 crore because they were the compliance officer under Regulation 6 of the LODR and did not address the violations,” said Vasani, adding that apart from directors, company secretaries also need to meticulously look into non-compliance and point out the violations accordingly.

Regulation 6 of SEBI Listing Obligations and Disclosure Requirements (LODR) clearly outlines the obligations of a compliance officer. Some of the key obligations are listed below: The compliance officer of the listed entity shall be responsible for:

· Ensuring conformity with the regulatory provisions applicable to the listed entity in letter and spirit.

· Co-ordination with and reporting to the Board, recognised stock exchange(s) and depositories with respect to compliance with rules, regulations and other directives of these authorities in the manner specified from time to time.

· Ensuring that the correct procedures have been followed that would result in the correctness, authenticity, and comprehensiveness of the information, statements, and reports filed by the listed entity under these regulations.

(Write to us at legalipr@bombaychamber.com)

Related party transaction isn’t dirty, its abuse is

Related party transaction isn’t dirty, its abuse is

Bombay Chamber, Mumbai: Related Party Transactions (RPTs) are not inherently unethical business practices. Listed entities across industries engage in legitimate business transactions while adhering to the Listing Obligations and Disclosure Requirements (LODR) prescribed by the Securities and Exchange Board of India (SEBI). However, not all companies comply with both the letter and spirit of the law, and some have been misusing or abusing RPTs to benefit certain executives, individuals, or entities connected to the promoter group.

“One listed entity, which I will not name, engaged in numerous abusive related party transactions (RPTs) at the subsidiary level. This called for scrutiny and corrective measures by SEBI. During the process, the regulator discovered that some transactions, while not involving a related party as the counterparty, ultimately aimed to benefit a related party. Consequently, SEBI introduced a purpose and effect test from April 1, 2023, in the RPT regulatory architecture, particularly for listed companies,” said Bharat Vasani, Chairperson, Legal Affairs & IPR Committee, Bombay Chamber of Commerce & Industry and Senior Advisor – Corporate Laws at Cyril Amarchand Mangaldas. Vasani was speaking at a Related Party Transaction (RPT) seminar held recently by the Bombay Chamber of Commerce & Industry in Mumbai.

In December 2024, a listed company transferred its business-to-consumer (B2C) business to its chief executive officer, who was also the promoter’s son. This was seen as a related party transaction, prioritising personal gain over shareholder interests and raising concerns about governance and transparency. Eventually, the son had to fund the new venture on his own, with the listed entity retaining a minority stake in the new B2C venture.

Legal industry experts cited another incident of gross violation of RPT regulatory architecture by a listed company (name withheld). When the regulator summoned one of the independent directors in question, the person pleaded ignorance of the Companies Act and the LODR, claiming to be just a physiotherapist of the promoter.

There have been numerous instances of gross violations in the past, including one involving one of the country’s largest airlines, which is no longer in existence. The airline had inducted a famous Bollywood lyricist as a board member who had no understanding of corporate business practices. While one might believe there is a difference between a habitual defaulter and a one-time defaulter, it is an open secret that there is none.

Corporate counsels believe that SEBI’s definition of related party transactions is very fluid and has been complicated by merging the concepts of ‘related party’ and ‘conflict of interest.’ As a result, they no longer understand the difference between the two concepts.

“Related party is not a bad term but is perceived as such. I think it’s just the conflict of interest aspect that should be dealt with carefully and hence needs to be regulated,” said Rajendra Chopra, Company Secretary/Compliance Officer at Cipla. “If you look at the entire Tata Group, their various business verticals work with other group companies, and it’s actually seen as a strength of the organisation,” he added.

Chopra pointed out that the regulator (SEBI) looks at RPTs in isolation. For example, a subsidiary was misused by IL&FS, DHFL, or other listed entities, hence the need to cover subsidiaries. The regulator needs to understand that it was not the regulation but the enforcement that was the problem in most cases.

“The regulator isn’t addressing the fundamental issue. So rather than strengthening their enforcement, they strengthen the regulation, thus laying down further regulations. Now they have introduced the purpose and effect test, thereby expanding the definition of a related party transaction,” said Chopra, adding that despite such measures, the regulator will not be able to control the fraud that can happen tomorrow.

Legal industry experts are also of the view that the LODR has not been aptly drafted. It leaves a lot of ambiguities in interpreting everything. As per a senior corporate lawyer, despite persistent requests from trade bodies, SEBI has not yet released frequently asked questions for LODR, unlike for Prohibition of Insider Trading (PIT) Regulations. “FAQs for LODR would have resolved various interpretative issues,” the lawyer said.

(Write to us at legalipr@bombaychamber.com)

MSME Conclave 2025: Unlocking Global Opportunities for India’s MSMEs

MSME Conclave 2025: Unlocking Global Opportunities for India’s MSMEs

January 15, 2025

The Bombay Chamber of Commerce and Industry (BCCI) hosted the MSME Conclave 2025: Global Opportunities for MSMEs on January 15, 2025, bringing together industry experts, policymakers, and international representatives to discuss strategies for empowering micro, small, and medium enterprises (MSMEs) through global market integration and export facilitation.

Setting the theme of the event, R. Srinivasan, Co-Chairperson of the MSME Forum and Director of AIRA Consulting Private, underscored the pivotal role of MSMEs in contributing 30% to India’s GDP and 40% to its exports. He highlighted the critical need to align MSMEs with the government’s ambitious vision of Viksit Bharat by 2047, emphasising on the importance of global market integration for sustained high growth.

The conclave featured three key sessions. The session on finance for exports featured presentations by prominent financial institutions. C. S. Arya, General Manager at IDBI Bank; Shirish Mathur, Head of SME Products & Digital Platforms at Aditya Birla Finance and Dhrubashish Bhattacharya, Head of MSME & Co-Lending at Bank of Baroda, elaborated on the services their banks were offering to MSMEs. Ratul Mukhopadhyay, Business Head of SEG Assets at Axis Bank and Vikas Kumar, Chief Manager at SBI SME Sakinaka Branch also highlighted customised banking solutions for exporters.

Addressing the session on Bilateral Growth: Advancing US-India Trade & Investment Potential, Joe Yang from U.S. Commercial Service, United States Consulate, Mumbai, detailed strategies for advancing US-India trade and investment ties, emphasising the potential of MSMEs in strengthening bilateral relations.

The session on bilateral trade opportunities included engaging presentations by consular experts. H. E. Adolfo Garcia Estrada, Consul General of Mexico, Eva Nilsson, Deputy Consul General of Finland, Dina Albahey, Vice Consul of Egypt and Viraj Kulkarni, Honorary Consul of the Republic of Cyprus.

The Conclave ended with a vote of thanks by Rajan Raje, Chairperson of the MSME Forum and CEO of Nichem Solutions. The event was supported by Aditya Birla Capital Ltd, Bank Of Baroda, Ashwin Sheth Group, Axis Mutual Fund and SBI Mutual Fund.

Bombay Chamber seminar discusses recent amendments to LODR and issues with Related Party Transaction regime

Bombay Chamber seminar discusses recent amendments to LODR and issues

with Related Party Transaction regime

Mumbai

Corporate India has been faltering on Related Party Transaction (RPT) despite numerous amendments to the Listing Obligations and Disclosure Requirements (LODR) by the Securities and Exchange Board of India (SEBI). While the entire architecture of the LODR has been significantly revamped and tightened further over the past decade, amendments are being made continuously with the recent one being announced on December 12, 2024.

To discuss and understand these changes, the Bombay Chamber of Commerce & Industry (BCCI) held a seminar on January 15, 2025, which saw participation from corporate law professionals and legal/compliance officers from across industries.

Addressing the gathering, Bharat Vasani, Chairperson Legal Affairs & IPR Committee, Bombay Chamber of Commerce & Industry and Senior Advisor – Corporate Laws, Cyril Amarchand Mangaldas, said the corporate sector will see further tightening of LODR in 2025. “SEBI is working on this aggressively. Significant changes will be announced very soon and the reasons (for these changes) are not far to seek,” said Vasani.

While there are companies that are legally compliant with the letter of the law and spirit, there are exceptions as well, and SEBI goes by legislating for the exception. “If they (SEBI) find a very abusive RPT, they immediately try to identify the loophole being missed and corrective actions are taken. As a result, the entire regulatory architecture, after comparing it internationally with other jurisdictions, I’d say that our regime is the toughest and most comprehensive in terms of disclosures and approvals,” said Vasani adding that the regime has been tightened from April 2023 leaving no loopholes.

Experts from the legal fraternity are of the view that a significant widening of the definition of Related Party Transactions (RPTs) back in 2022, in a manner far beyond what was in Section 2(76) in the Companies Act, 2013, has at times made it very challenging for legal and compliance officials across listed entities to conduct day-to-day operations in their respective businesses. And SEBI has its reasons to do so because public money is at play and hence the need to be tightly regulated.

Highlighting the key amendments (SEBI notification, effective December 12, 2024) to the provisions concerning RPTs Geetika Anand, Joint President, Company Secretary and Compliance Officer, Hindalco Industries (Aditya Birla Group), said there are five areas primarily that need to be looked at in particular. “Specific exclusions from the definition of RPT, current/saving account approval for RPTs for remuneration and sitting fees, ratification of RPTs, omnibus approval for subsidiary’s RPTs and finally exemption from approval requirements, these are quick five major RPT amendments,” said Anand while also explaining the rationale behind each of the amendments.

This was followed by an engaging discussion between the panel members and legal industry professionals in the audience.

Majority of the queries revolved around 2024 amendments made in December 2024, particularly on the ratification of transactions by the audit committee, concerning missing approvals for transactions above Rs 1 crore and refusal by the audit committee to ratify it. Responding to the queries Rajendra Chopra, Company Secretary/Compliance Officer, Cipla, said, the provision of Section 22F regarding ratification, says that the audit committee may ratify the transaction.

Explaining further, Chopra talked about two scenarios viz. transaction being executed with approval and a second transaction is approved by the audit committee but the amount of transaction was more than what was being approved.

“Can we call both transactions as ratification or just the transaction that wasn’t approved at all, as ratification? In my opinion, as long as the transaction is approved by the audit committee but the amount has incidentally exceeded, I will not qualify that as ratification. However, if the transaction was not approved at all, I will consider that as ratification. That’s my personal view / interpretation of the scenario,” said Chopra.

On possible violations in the aforesaid scenario, Chopra said it’s not a ratification if the audit committee has already approved the transaction and the company executes it despite transaction exceeding the approved amount. “In my opinion, the transaction is already got comprehensive approval from the audit committee and it’s only the amount (just one of the components) that’s changed. So I’ll not categorise it as ratification. Having said that, the audit committee enjoys all inherent power and is free to reject the transaction and levy a penalty as per internal guidelines,” said Chopra.

In her closing remarks, Attreyi Mukherjee, Co-Chair of Legal Affairs and IPR Committee at the Bombay Chamber of Commerce and Industry and General Counsel, Tata Industries Ltd, said it was a very interactive and engaging session. “For the various nuances this subject has, especially given the recent amendments whether it was the topic of ratification or calculation of royalty payments, which I think sparked a very lively debate and deliberation,” said Mukherjee.

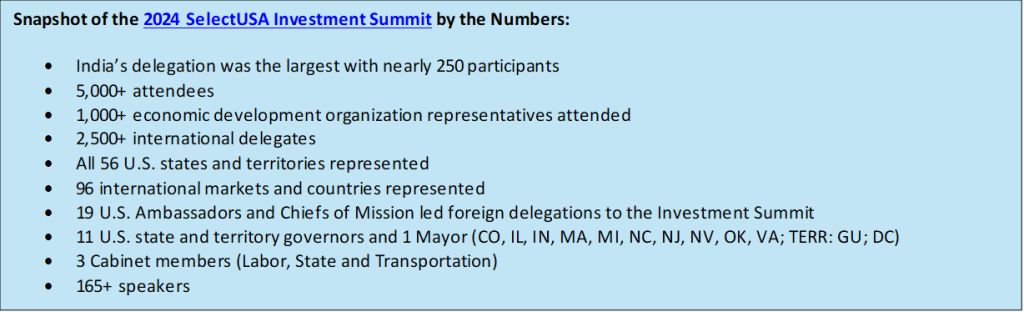

2025 Select USA Investment Summit

2025 Select USA Investment Summit

SelectUSA is the U.S. federal government program dedicated to attracting and retaining investment in the U.S. economy. This program is dedicated to facilitating and promoting impactful business investment into the United States to create jobs, spur economic growth, and promote U.S. competitiveness.

Since its inception, SelectUSA has assisted thousands of clients, including economic development organizations (EDOs), domestic firms, and international companies, facilitating over $200 billion in client-verified investment, supporting more than 200,000 jobs across the United States and its territories.

Every year, the U.S. Department of Commerce hosts its Annual Investment Summit. The 2025 SelectUSA Investment Summit will take place May 11-14, at the Gaylord National Resort and Convention Center in National Harbor, MD.

The SelectUSA Investment Summit is the premier event in the United States for FDI promotion. Investment Summit attendees can expect to:

- Forge partnerships and connect with economic developers from 50+ states and territories, companies from 90+ markets, speakers, government officials and more; set up one-on-one or group meetings and make your investment deals happen.

- Gain advice and information from policy and industry experts in more than 50 sessions providing you with actionable instruction on everything from developing a workforce to understanding incentives.

- Explore the Exhibition Hall featuring economic development organizations, service providers, industry experts, and international tech startups.

The SelectUSA Investment Summit draws more than 5,000 attendees! You can expect to meet EDOs representing the U.S. states and territories, more than 2,500 business investors with representation from 90+ international markets, and industry experts who will provide insight and advice on how to make your move to the U.S.!

We hope you will consider joining the 2025 Investment Summit and take advantage of year’s event the best yet!

APPLY NOW to attend the biggest FDI event of 2025 : www.selectusasummit.us