If the disciplinary authority accepts the findings recorded by the enquiry officer, no detailed reasons are required to be recorded in the order imposing punishment. – Supreme Court

Blog

If the disciplinary authority accepts the findings recorded by the enquiry officer, no detailed reasons are required to be recorded in the order imposing punishment. – Supreme Court

If the disciplinary authority accepts the findings recorded by the enquiry officer and passes an order, no detailed reasons are required to be recorded in the order imposing punishment.

Copy of judgement attached.

Procurement Notice–State Pharmaceuticals Corporation of Sri Lanka

Procurement Notice–State Pharmaceuticals Corporation of Sri Lanka

I wish to inform you that, the State Pharmaceuticals Corporation of Sri Lanka has invited sealed bids for supply of following items to the Ministry of Health.

| Bid Number | Closing Date & Time | Item Description | Non – refundable Bid Fee

(in LKR) |

| DHS/P/C/WW/10/25 | 10.02.2025

at 10.00 A.M. |

500,000 PFSY of Enoxaparin sodium injection 6,000IU/0.6ml

PFSY/vial. |

Rs. 500,000/=

+ Taxes |

| DHS/P/C/WW/11/25 | 10.02.2025

at 10.00 A.M. |

2,200,000 vials of Biphasic Isophane Insulin Injection (Human) 30% soluble/70%Isophane. | Rs. 500,000/=

+ Taxes |

Please find attached herewith a copy of the procurement notices of the above.

It would be appreciated, if you could kindly make necessary arrangements to disseminate the same among your membership.

Thank you.

With warm regards,

Shirani Ariyarathne

Actg. Consul General

Minister (Commercial)

Consulate General of Sri Lanka

34, Homi Mody Street, Fort

Mumbai 400001

Tel: (+ 91 22 )22045861/22048303

Fax: (+ 91 22) 22876132

E -mail: slcg.mumbai@mfa.gov.lk

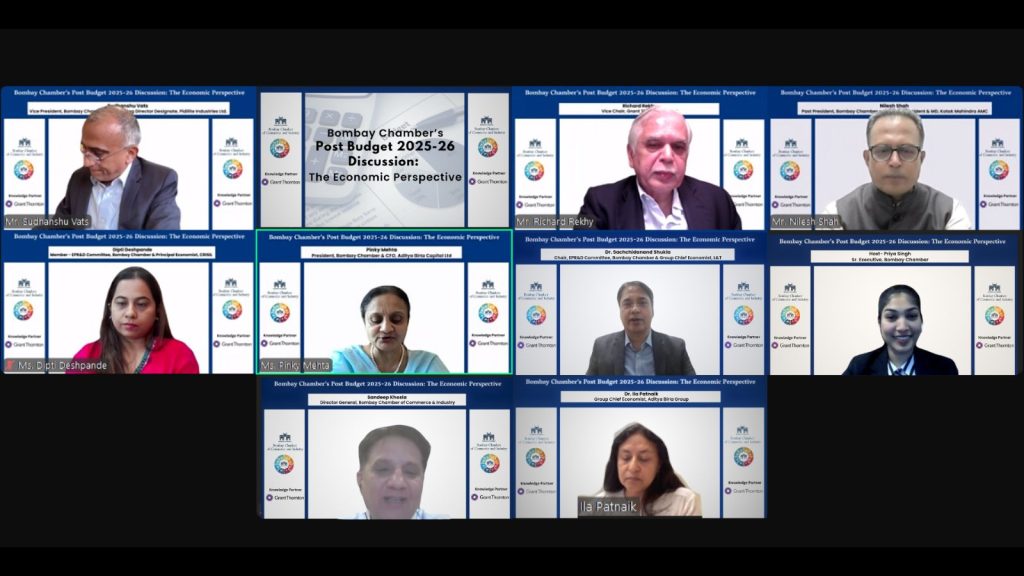

Bombay Chamber Hosts Post-Budget 2025-26 Webinar: An Economic Perspective

Bombay Chamber Hosts Post-Budget 2025-26 Webinar: An Economic Perspective

Mumbai, February 4, 2025 – The Bombay Chamber of Commerce & Industry, under the aegis of its Economic Policy Research & Development (EPR&D) Committee hosted a post-budget discussion on the economic perspective following the Union Budget 2025-26, presented by Finance Minister Nirmala Sitharaman on February 1, 2025.

The webinar commenced with a welcome address by Pinky Mehta, President of the Bombay Chamber and CFO of Aditya Birla Capital Ltd., who highlighted the budget’s focus on strengthening private sector investments, boosting household sentiment, and enhancing middle-class purchasing power. She noted that Finance Minister Sitharaman reaffirmed the government’s commitment to inclusive growth through targeted initiatives for the poor, youth, farmers, and women, while also underscoring MSMEs as the “second engine” of the economy. Key budget highlights included the Prime Minister Dhan-Dhaanya Krishi Yojana, which aims to enhance agricultural productivity across 100 districts, and the announcement of five National Centres of Excellence for skilling, supporting India’s ambition to become a global manufacturing hub.

The panel discussion, moderated by Dr. Sachchidanand Shukla, Chair of the EPR&D Committee at the Bombay Chamber and Group Chief Economist at L&T, featured distinguished experts, including Dr. Ila Patnaik, Group Chief Economist at Aditya Birla Group; Nilesh Shah, Past President of the Bombay Chamber and Group President & MD at Kotak Mahindra AMC; Sudhanshu Vats, Vice President of the Bombay Chamber and Managing Director Designate at Pidilite Industries.; Dipti Deshpande, Principal Economist at CRISIL; and Richard Rekhy, Vice Chair at Grant Thornton Bharat.

Discussions focused on tax reforms, economic growth, fiscal discipline, and global trade. Shah highlighted the need for better tax compliance and expressed optimism for a more favourable tax regime in the coming years. Deshpande noted that despite tax relief measures, income tax collections are projected to grow by 20.6 percent, driven by structural changes, compliance, and digitalisation. She also highlighted the government’s commitment to fiscal prudence, noting that the fiscal deficit has been reduced to 4.4 percent and remains on track to fall below 4.5 percent in 2025-26. Revenue spending cuts, strong tax collections, and PSU dividends are key drivers of this fiscal consolidation, reinforcing India’s long-term economic stability.

Dr. Patnaik stressed the importance of removing the inverted duty structure to create a level playing field for Indian industries and noted that policy changes are advancing the Make in India initiative. Vats described the budget as balanced and forward-looking, citing the one lakh crore rupees tax rebate as a bold move to stimulate middle-class consumption and drive growth in manufacturing, services, and GST revenues. Addressing global trade concerns, Shah emphasised the need for India to engage in strategic partnerships to avoid negative impacts from ongoing trade tensions.

Rekhy pointed out that while middle-class spending is rising, challenges such as food inflation, underemployment, and regulatory complexities persist. He highlighted the importance of skilling initiatives to support India’s goal of becoming a global talent hub.

The panellists agreed that the Union Budget 2025-26 maintains a strong balance between fiscal prudence and economic growth, with continued policy implementation and regulatory reforms being key to sustaining long-term stability.The session concluded with a vote of thanks by Sandeep Khosla, Director General of the Bombay Chamber.

Uma Devi’s judgment does not justify the perpetual exploitation of daily wage workers denying them the benefits of regularization – Supreme court

Uma Devi’s judgment does not justify the perpetual exploitation of daily wage workers denying them the benefits of regularization – Supreme court

Uma Devi’s judgment does not justify the perpetual exploitation of daily wage workers denying them the benefits of regularization.

Copy of judgement attached

Ban On Fresh Recruitment No Excuse To Deny Benefits Of Regularization To Daily Wage Workers – Supreme Court

Ban On Fresh Recruitment No Excuse To Deny Benefits Of Regularization To Daily Wage Workers – Supreme Court

Ban On Fresh Recruitment No Excuse To Deny Benefits Of Regularization To Daily Wage Workers

Copy of judgement attached

One-sided, forfeiture clauses in builder-buyer agreements are “unfair trade practices” – Supreme court

One-sided, forfeiture clauses in builder-buyer agreements are “unfair trade practices” – Supreme court

One-sided, forfeiture clauses in builder-buyer agreements are “unfair trade practices.

Copy of judgement attached

Advocate cannot represent a workman in an enquiry where the Management Representative is not a legally trained person – Bombay HC

Advocate cannot represent a workman in an enquiry where the Management Representative is not a legally trained person – Bombay HC

Advocate cannot represent a workman in an enquiry where the Management Representative is not a legally trained person.

Copy of judgement attached

Writ Petition not maintainable against NBFC, Private Bank – Supreme Court

Writ Petition not maintainable against NBFC, Private Bank – Supreme Court

An entity being subject to regulatory guidelines under a statute does not automatically make it subject to Writ Jurisdiction.

Copy of judgement attached.

Supreme Court directs Government to consider the enactment of a law to protect the rights of domestic workers

Supreme Court directs Government to consider the enactment of a law to protect the rights of domestic workers

The SC have the following directions:-

“As regard to the larger issue of the protection of rights of domestic workers,we direct the Ministry of Labour and Employment in tandem with the Ministry of Social Justice and Empowerment, the Ministry of Women and Child Development, and the Ministry of Law and Justice, to jointly constitute a Committee comprising subject experts to consider the desirability of recommending a legal framework for the benefit, protection and regulation of the rights of domestic workers.”

Copy of judgement attached.

By: Raj Singh

No Comments

Budget 2025-26 empowers MSMEs, Middle class as engines for industrial growth

Budget 2025-26 empowers MSMEs, Middle class as engines for industrial growth

In her eighth consecutive Union Budget 2025-26, Finance Minister Nirmala Sitharaman delivered a Budget which reflected the government’s strategic focus on empowering MSMEs and implementing comprehensive reforms to foster industrial growth and economic development in India. The Budget also introduced historic income tax changes aimed at benefiting the middle class. This Budget seeks to invigorate private sector investments, uplift household sentiments, and strengthen the purchasing power of India rising middle class, the finance minister stated.

In her address, Sitharaman outlined the government focus on ten key areas of development, emphasising support for the poor (Garib), youth (Yuva), farmers (Annadata), and women (Nari). Sitharaman also recognised MSMEs as the second engine of the economy, highlighting their significant role in India industrial growth. Currently, over one crore registered MSMEs contribute 37% of manufacturing output and 45% of exports, positioning India as a global manufacturing hub.

Reactions from Bombay Chamber Leaders:

Pinky Mehta, President Bombay Chamber and CFO of Aditya Birla Capital Ltd:

This Budget has a focus on double ‘M’ – MSMEs and the Middle Class. The investment limit for MSMEs has been raised by 2.5 times, reflecting the government’s commitment to strengthening this sector. This move will encourage higher capital investment and expansion among MSMEs. Moreover, a significant increase in the credit guarantee cover for MSMEs, doubling it from ₹5 crore to ₹10 crore, is expected to facilitate an additional ₹1.5 lakh crore in credit over the next five years, thereby improving access to finance for small businesses. The relief for the Middle class with no income tax payable up to ₹12 lakh under the new tax regime is expected to increase disposable income, thereby stimulating demand across various sectors, including FMCG and the automotive industry.

Rajiv Anand, Sr. Vice President, Bombay Chamber and Deputy Managing Director, Axis Bank:

The path to fiscal consolidation is welcome. The income tax cut will help the middle class and consumption.

Sudanshu Vats, Vice President, Bombay Chamber and Managing Director Designate, Pidilite Industries Ltd.

I would like to compliment Hon Finance Minister for a good balanced budget with clear focus on driving consumption while staying the course on fiscal consolidation. The two key features have been reduction in personal Income Tax leaving more money in the hands of Indian consumers and the introduction of PM Dhan Dhaanya Krishi Yojana for 100 districts – a more holistic approach to address the Agriculture sector.

Nilesh Shah, Past President, Bombay Chamber and Group President & MD, Kotak Mahindra AMC Ltd:

The budget delivers on the expectations of Triveni sangam of reduction in fiscal deficit, support to urban consumption through tax cuts and increase in Capex through center, state and PSUs allocation. The budget is forward looking with six year guidance on reducing debt to GDP ratio, allocation to deep tech fof of Rs 10,000 crore, maritime fund of Rs 25000 crore for ship buildingand Rs 20000 crore For small modular nuclear reactors and Focus on Education through digital books, broadband connectivity, increase in medical and IIT seats and Atal tinkering labs.

Sudhir Kapadia, Past President Bombay Chamber and Senior Advisor, EY

This budget has given one of the most expansive giveaways on the personal income tax front, with the government foregoing an unprecedented Rs 1 lakh crore in direct tax revenues. With this, the government has shown that it is listening to the middle class voices. This will also bring about a spurt in disposable income, benefiting the economy. The big announcement on the new income tax bill that will be introduced next week is much welcome. The new bill will be simpler and easier for taxpayers to understand. The formation of a high level panel for Regulatory Reforms to review regulations, certifications, licences, and permissions in the non- financial sector is another signal that we are open to business.

Key Highlights of the Budget 2025-26

Economic Growth & Development

● India remains the fastest-growing major economy.

● The budget prioritises accelerated growth and inclusive development.

● Emphasis on private sector investments and enhanced household confidence.

10 Focus Areas

● Prioritising Garib (poor), Yuva (youth), Annadata (farmers), and Nari (women).

● Focus on taxation, urban development, mining, financial sector, power, and regulatory

reforms.

Agriculture & Rural Development

● PM Dhan Dhaanya Krishi Yojana to improve agricultural productivity in 100 low-yield

districts.

● Expansion of storage infrastructure at the panchayat level.

● Special initiatives for pulse crops (urad, tuar, masoor).

● Establishment of a Makhana Board in Bihar to boost local production.

MSME & Industrial Growth

● Investment and turnover limits for classification will be enhanced by 2.5 times, encouraging expansion and employment generation.

● Credit guarantee cover will be increased from ₹5 crore to ₹10 crore for micro-

enterprises, leading to an additional ₹1.5 lakh crore in credit over the next five years.

Healthcare & Education

● 75,000 new undergraduate medical seats to be added in the next five years.

● Day-care cancer centers to be established in all district hospitals.

● 50,000 Atal Tinkering Labs to be set up in government schools.

Infrastructure & Logistics

● India Post to be transformed into a major public logistics organisation.

● New urea plant in Assam with a capacity of 12.7 lakh metric tons.

● Reactivation of three dormant urea plants in Eastern India.

Entrepreneurship & Women Empowerment

● ₹2 crore term loan scheme for 5 lakh first-time women, SC, and ST entrepreneurs.

● MSME credit guarantee cover expanded to ₹20 crore, with reduced guarantee fees.

Technology & Innovation

● Establishment of the National Institute of Food Technology, Entrepreneurship, and

Management in Bihar.

● Bharatiya Bhasha Pustak Scheme to promote Indian language digital books for

education.

● Five national skilling centers to support the ‘Make for India, Make for the World’

initiative.

Energy & Sustainability

● Nuclear Energy Mission targets 100 GW of nuclear energy by 2047.

● Amendments to the Atomic Energy Act to facilitate private sector participation.

Social Welfare & Financial Inclusion

● Enhanced support for gig and online platform workers via identity cards and the e-

Shram portal.

● Revamped PM SVANidhi scheme with higher loan limits and UPI-linked credit cards for

street vendors.