Restrictive covenant prescribing a minimum tenure of service is not in restraint of trade or opposed to public policy.

Copy of judgement attached

Restrictive covenant prescribing a minimum tenure of service is not in restraint of trade or opposed to public policy.

Copy of judgement attached

Ref.: MCM/ADM/11 14 May 2025

The Director General

Bombay Chamber of Commerce and Industry

Mackinnon Mackenzie Building

3rd floor, 4, Shoorji Vallabhdas Road

Ballard Estate, Mumbai – 400 001

Dear Sir/Madam,

Invitation for Bids

Please see enclosed notices for invitation for bids from organizations in Mauritius.

Prospective bidders may be requested to regularly visit the website to take cognizance of any addendum and/or clarification(s) issued.

The Consulate would highly appreciate if you could kindly circulate the Notices among the members of your Organization.

Thank you for your understanding and cooperation.

Yours sincerely,

D. K. Bucktowar

Consul and Head of Mission

Consulate of the Republic of Mauritius

1107, Regent Chambers

11th Floor, Jamnalal Bajaj Marg

208, Nariman Point

Mumbai – 400 021

Tel. : 022 22825421 /22

Invitation for Bids (IFB) – Department of Immigration & Emigration

IFB No. – DIE/PRO/PKI/2025 – Procurement of Issuance System and Relevant Public Key Infrastructure Components for Personalization of e-Passports to the Department of Immigration & Emigration of Sri Lanka

I wish to inform you that, the Chairman, High Level Procurement Committee (HLPC) on behalf of the Department of Immigration and Emigration has invited sealed bids from eligible bidders for the Procurement of Issuance System and Relevant Public Key Infrastructure Components for Personalization of e-Passports to the Department of Immigration & Emigration of Sri Lanka.

All bids must be accompanied by a Bid Security in the form of bank guarantee of not less than Sri Lankan Fifty Five Million (LKR 55 Million) or the equivalent amount in a freely convertible currency in Sri Lanka.

Closing date for the submission of above is on or before 23rd June 2025 at 03.00 pm (Sri Lanka local time GMT+5:30).

Please find attached herewith a copy of the procurement notice of the above.

It would be appreciated, if you could kindly make necessary arrangements to disseminate the same among your membership.

Tel: (+ 91 22 )22045861/22048303

Fax: (+ 91 22) 22876132

E -mail: slcg.mumbai@mfa.gov.lk

In a landmark move marking a new chapter in global commerce, India and the United Kingdom have successfully concluded a Free Trade Agreement (FTA), bringing an end to years of negotiations. The deal, hailed as a ‘historic milestone’ by Prime Minister Narendra Modi, is expected to significantly enhance bilateral trade, create new job avenues, and boost economic growth.

For India, the agreement presents both opportunities and challenges. While it opens doors for increased exports and foreign investment, it also raises concerns about domestic industries facing heightened competition. The deal is expected to catalyse trade, investment, and innovation, but its long-term impact on India’s economy remains to be seen.

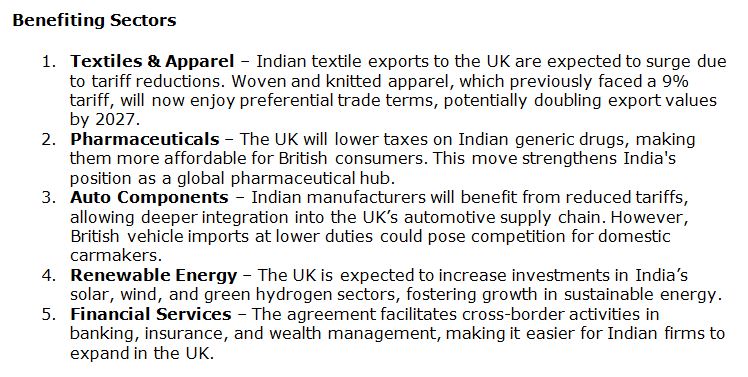

One of the most significant advantages of the FTA is the elimination or reduction of tariffs on a wide range of goods and services. Indian exporters, particularly in labour-intensive sectors such as textiles, footwear, and automobile components, stand to benefit immensely. The UK has agreed to eliminate tariffs on these products, making Indian goods more competitive in the British market.

Additionally, the agreement includes provisions for increased mobility of skilled Indian professionals to the UK, particularly in sectors such as information technology (IT) and healthcare. The Double Contribution Convention, a social security pact, ensures that Indian workers in the UK and their employers are exempt from paying social security contributions for three years, reducing financial burdens and enhancing employment opportunities.

The pharmaceutical and medical device industries are also expected to see a surge in exports, as the UK lowers tariffs on these products. With India being a global leader in generic medicines, this move could significantly boost revenue for Indian pharmaceutical firms.

While the agreement offers numerous benefits, it also presents challenges for certain Indian industries. The reduction of tariffs on British whisky and gin, for instance, has raised concerns among domestic beverage manufacturers. Indian tariffs on these products will be halved from 150% to 75%, and further reduced to 40% over the next decade. This could lead to increased competition for Indian liquor brands, potentially impacting local businesses.

Similarly, the automotive sector faces mixed outcomes. While Indian manufacturers will benefit from reduced tariffs on exports, the influx of British automobiles at lower duties could pose a challenge for domestic carmakers. The UK has negotiated a tariff reduction from 100% to 10% under a quota system, which may lead to increased imports of British vehicles.

Agriculture remains another sensitive area. India has excluded certain agricultural products, such as dairy, apples, and cheese, from duty concessions to protect its farmers. However, concerns persist about the potential impact of increased competition from British agricultural exports.

The FTA is expected to have a positive impact on India’s gross domestic product (GDP) growth, with projections indicating a substantial increase in bilateral trade. The British government estimates that trade between the two nations will rise by £25.5 billion annually from 2040 onwards. This surge in trade is likely to contribute to India’s economic expansion, fostering job creation and investment.

Moreover, the agreement strengthens India’s position as a global trade partner, reinforcing its commitment to economic liberalisation. By opening up key sectors and reducing trade barriers, India is positioning itself as a flexible and attractive destination for foreign investment.

(Write to us at editorial@bombaychamber.com)

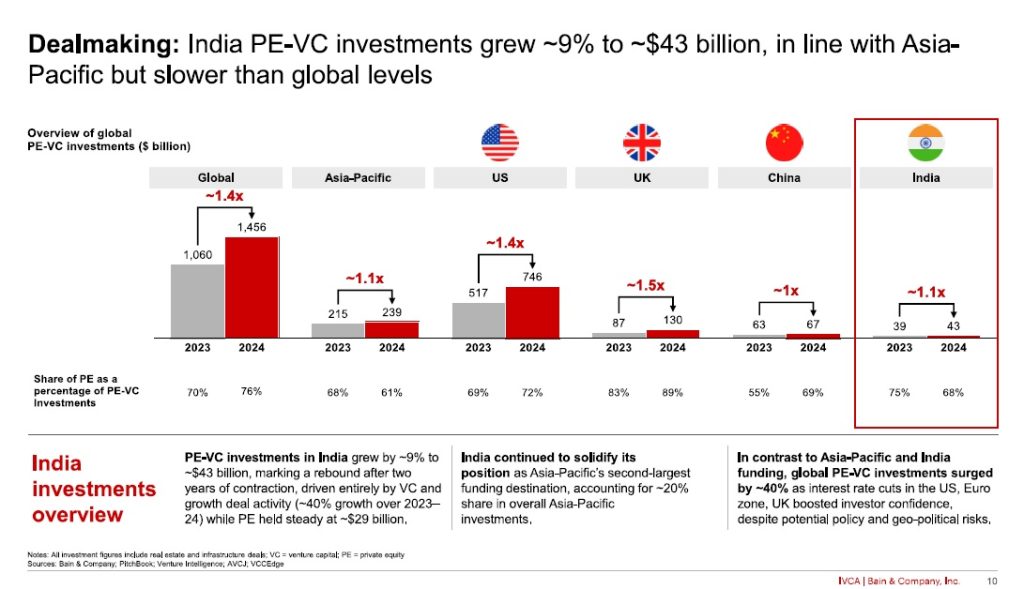

India’s private equity and venture capital (PE-VC) market rebounded strongly in 2024, reversing two years of contraction with a 9% rise in investments to reach $43 billion across 1,600 deals. As Asia-Pacific’s second-largest PE-VC hub, India continues to attract global capital, signalling renewed investor confidence in its macroeconomic stability and long-term growth potential.

According to Bain & Company’s ‘India Private Equity Report 2025’, published in collaboration with the Indian Venture and Alternate Capital Association (IVCA), while growth-stage investments drove much of the resurgence, private equity remained steady at $29 billion. A major shift towards buyouts was evident, with their share of total PE activity surging to 51% from 37% in 2022. Investors are increasingly securing control positions in high-quality assets, leveraging record dry powder reserves to pursue scalable opportunities.

Real estate and infrastructure emerged as standout performers, collectively accounting for 16% of total PE-VC funding, with deal values soaring by 70% compared to the previous year. Financial services also experienced robust growth of 25%, particularly within non-banking financial companies (NBFCs), driven by affordable housing finance, micro-lending, and MSME financing. Large transactions in companies such as Shriram Housing Finance and Aavas Financiers underscore investor confidence in high-yield, asset-secured businesses.

The healthcare sector maintained strong momentum, with an 80% increase in deal volume. Investments in medical technology, pharmaceutical outsourcing, and single-specialty hospitals – particularly in areas like eyecare, oncology, and IVF – highlighted a strategic push towards underpenetrated categories.

Meanwhile, IT-enabled services saw remarkable expansion, with deal activity tripling. Notable transactions such as Perficient’s $3 billion deal, Altimetrik’s $900 million investment, and GeBBS’s $865 million acquisition reinforced the sector’s growing dominance in digital transformation and revenue cycle management.

India also led the Asia-Pacific region in private equity exits, with exit values reaching a record-breaking $33 billion across 360 deals, marking a 16% year-over-year increase. Public market exits gained prominence, making up 59% of total exit value compared to 51% in 2023, as strong IPO activity fuelled investor optimism. The IPO landscape expanded significantly, with 33 listings in 2024 – up from 23 the previous year – driven largely by consumer-focused sectors.

Domestic fundraising hit new highs, further strengthening India’s private capital ecosystem. Kedaara Capital closed a landmark $1.7 billion fund, while ChrysCapital raised a record $2.1 billion. Global funds also intensified their presence, with Blackstone announcing plans to double its India-based assets under management from $50 billion to $100 billion, reflecting growing international confidence in India’s economic trajectory.

The private equity and venture capital market in India rebounded in 2024 and the outlook for 2025 remains positive. However, sustaining the momentum will require funds to navigate shifting economic and market conditions. Investors with strong operational capabilities, sector-specific expertise, and a focus on sustainable value creation will be best positioned to capitalise on opportunities. As the market tilts towards traditional industries and domestic fundraising reaches new highs, India’s PE-VC landscape looks set for a steady and long-term growth.

(Write to us at editorial@bombaychamber.com)

When charges, evidence, witnesses and circumstances in criminal proceedings and a disciplinary proceeding are identical or substantially similar dismissal would be unjustified

Copy of judgement attached.

Disciplinary proceedings cannot be continued beyond time specified by the Court without seeking extension

Copy of judgement attached

The Bombay Chamber of Commerce and Industry hosted its PEVC Conclave on the theme “Future of Fund Management: AIFs in GIFT City.” The event brought together fund managers, policymakers, regulators, and industry experts to explore the growing significance of GIFT City and its role in shaping India’s financial services landscape.

The conclave opened with a welcome address by Sandeep Khosla, Director General of the Bombay Chamber, who outlined the Chamber’s wide-ranging initiatives and reaffirmed its longstanding role as a bridge between industry and government. He emphasised the importance of fostering collaborative dialogue to support India’s evolving financial ecosystem.

Setting the theme of the Conclave, Ashith Kampani, Chair of the PE&VC Committee at the Bombay Chamber and Chairman of CosmicMandala15 Securities highlighted the Chamber’s focus on collaborative development toward a Viksit Bharat, grounded in digitalisation, ESG integration, ease of doing business, and inclusive growth—principles reflected throughout the day’s discussions. Kampani underscored how these pillars are directly relevant to the evolving financial landscape in GIFT City, India’s first operational smart city and International Financial Services Centre (IFSC). He highlighted the momentum GIFT City has gained, with over 80 fund managers operating within its ecosystem and more than $20 billion in fund commitments, as evidence of its growing prominence. He also noted that the progressive regulatory framework, especially following the introduction of the Fund Management Regulations in 2022, offers unparalleled flexibility in fund structuring, cross-border investments, and tax incentives—making GIFT City a highly attractive jurisdiction for global capital and investment innovation.

Swati Khemani, Founder and CEO of Carnelian Asset Management & Advisors, delivered the keynote address. She emphasised that GIFT City represents a transformational shift in India’s financial sector, offering regulatory transparency, tax incentives, and infrastructure that rival global standards. With over $36 billion in assets under management and 124 registered fund units as of March 2024, GIFT City is becoming a preferred destination for asset and wealth managers worldwide.

Khemani also connected GIFT City’s evolution with the government’s broader vision under Amrit Kaal, projecting India’s share in global trade to rise from 12 percent to 16 percent and targeting per capita income of $18,000. She noted the city’s multi-currency capabilities, favorable tax treatment, and appeal for non-resident investors as key differentiators, positioning GIFT as a global center for financial innovation.

The first panel discussion, titled GIFT AIFs: Unlocking Inbound and Outbound Investment Potentials, was moderated by Tejas Desai, Co-Chair of the PE&VC Committee at the Bombay Chamber and Partner at Ernst & Young. The panellists included Pavan Shah, General Manager, International Financial Services Centres Authority (IFSCA); Mitul Mehta, Chief Financial Officer, Blume Ventures; Lakshmi Iyer, CEO – Investment & Strategy, Kotak Alternate Asset Managers; Clarence Anthony, Managing Partner, Clarence & Partners; and Niutpol Handique, Assistant Vice President – International Business Development, Mirae Asset Management Company.

The session addressed the game-changing nature of 100 percent NRI-focused funds, the challenges faced by domestic SEBI AIFs in making offshore investments, and how the FEMA non-resident status of GIFT AIFs offers a compelling solution. The discussion also covered recent amendments to the Fund Management Entity Regulations and the tax advantages of launching asset-specific funds through GIFT City, especially for investing in Indian mutual funds.

The second panel, Dual Listing in GIFT City, moderated by Jyoti Vineet Tandon, Compliance Consultant and Co-Founder of FinCrimeExpert, featured Pradeep Ramakrishnan, Executive Director, International Financial Services Centres Authority (IFSCA); Vijay Krishnamurthy, Managing Director and CEO, India INX; Siddharth Shah, Partner, Khaitan & Co.; and Veenit Surana, Partner, Ernst & Young. The panellists provided insights into IFSCA’s regulatory vision, the readiness of market infrastructure institutions, and the broader ecosystem required to make dual listings a viable and attractive route for Indian and global market participants.

The event concluded with a vote of thanks from Sandeep Khosla who underscored the value of the discussions and the Chamber’s ongoing efforts to support industry-policy collaboration.

For More Details Contact: Priya Singh at priya.singh@bombaychamber.com OR 022 61200238

Pune, April 21, 2025 – In a landmark initiative to revolutionize the agriculture sector through innovation and technology, Pune will host the country’s first-ever International Agritech Hackathon. The event was officially launched on 21st April 2025 by Hon’ble Guardian Minister (Pune) and Deputy Chief Minister of Maharashtra State, Shri Ajit Dada Pawar, at Ganesh Kala Krida Manch, Pune.

The International Agritech Hackathon is a collaborative effort between the District Administration, Pune, and the Bombay Chamber of Commerce & Industry. During the launch, a MoU was signed by Mr. Jitendra Dudi, District Collector, Pune and Chief Organizer of the Hackathon, Mr. Rajan Raje, Chairperson, Agriculture & Food Processing Committee – Bombay Chamber and CEO, Nichem Solutions and Mr. Chetan Dedhia, Expert Committee Member, Agriculture & Food Processing Committee – Bombay Chamber and Managing Partner, J.J.Overseas.

Through this MoU, the Bombay Chamber has extended full support to the district administration to ensure the successful execution of the Hackathon.

The International Agritech Hackathon aims to bring together students, startups, developers, researchers, and innovators from diverse backgrounds, all driven by a shared goal — to transform the future of agriculture through cutting-edge technology.

Registrations are now open, and interested participants can register via the official website: https://www.puneagrihackathon.com/